The Law of Demand says……Consumers will buy more when prices go down and less when prices go up.

BUT …….

HOW MUCH MORE OR LESS?

Does it really matters?

Elasticity is ……..

- is a measure of how much buyers and sellers respond to changes in market conditions.

- It allows us to analyze supply and demand with greater precision.

Price elasticity of demand

- is the responsiveness of consumers to a change in the price of a product. Shows how sensitive consumers are to a change in price.

- The price elasticity of demand is computed as:

Ed= Percentage in quantity demanded

Percentage change in price

Ed= ∆ in Q ÷ ∆ in P

Q P

- Be sure to use absolute values and ignore the — sign; useful for comparing different products.

Interpretation of Ed:

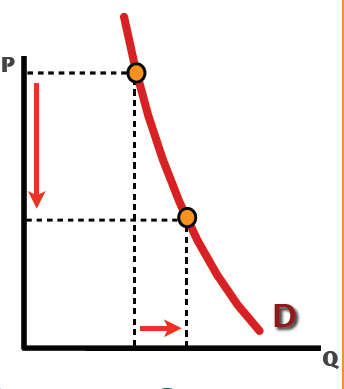

- Inelastic Demand = INSENSITIVE TO A CHANGE IN PRICE. Percentage change in price is greater than the percentage change in quantity demanded.In other words,people will continue to buy it! Ed: is less than one.

- An Inelastic Demand curve is STEEP! …… The STEEPER the curve the MORE INELASTIC the Demand.

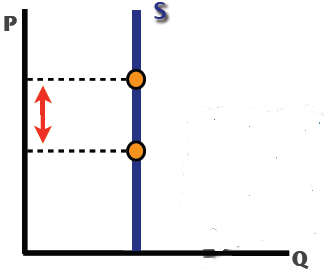

- Perfectly Inelastic—‰ Quantity demanded does not respond to price changes at all.

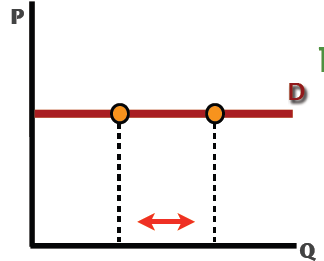

- Elastic Demand = SENSITIVE TO A CHANGE IN PRICE. Percentage change in quantity demanded is greater than the percentage change in price. In other words, price plays a Huge role! Ed: is more than one.

- An Elastic Demand curve is FLAT! ……. The FLATTER the curve the MORE ELASTIC the Demand

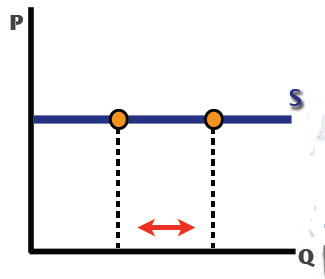

- Perfectly Elastic—‰ Quantity demanded changes infinitely with any change in price.

- Unit Elastic = Percentage change in quantity demanded is equal to the percentage change in price. Ed: is equal to one.

- In other words, a 10% drop in price causes a 10% increase in quantity demanded.

Demand tends to be more elastic . . .

- if the good is a luxury.

- the longer the time period.

- the larger the number of close substitutes.

- the more narrowly defined the market.

Demand tends to be more inelastic . . .

- if the good is a necessity.

- the shorter the time period.

- the fewer the number of close substitutes.

- the more broadly defined the market.

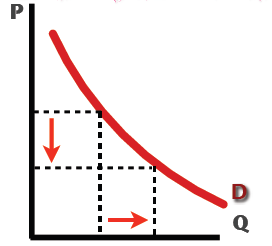

Elasticity Varies with Price Range—more elastic toward top left; less elastic at lower right

Total Revenue Test for Elasticity

- Total Revenue is the amount the seller receives from the buyer from the sale of a product; P x Q = TR

- Elasticity and total revenue are related; observe the effect on total revenue when product price changes

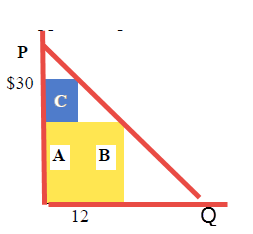

In 2000 people purchased about 20 million videos of Walt Disney’s Jungle Book at a price of about $25.

Total Revenue (A & B) was $500 million.

- Suppose the price increases, causing Q to drop.

- Now TR is A & C and is C equal to $360 million.

- If demand is elastic, then a decrease in price will increase total revenue; an increase in price will decrease total revenue.

- If demand is inelastic, then a decrease in price will reduce total revenue; an increase in price will increase total revenue.

- If demand is unit elastic, any change in price will leave total revenue unchanged.

Other Demand Elasticities

Income elasticity of demand measures the responsiveness of demand to change in income as

Income elasticity =% change in quantity demanded

% change in income

A good with a positive income elasticity is known as Normal good. In this case, as income rises, demand also rises.

A good with negative income elasticity is an Inferior good. In this case, as income rises, demand falls.

Cross price elasticity of demand measures the responsiveness of quantity demanded of one good (good x) with a change in price of another good (good y)

Cross price elasticity = % change in quantity demanded (x)

% change in price (y)

Cross price elasticity of demand is positive, then the goods are substitute.

Cross price elasticity of demand is negative, then the goods are compliments

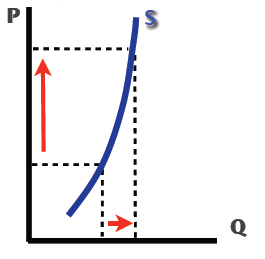

Elasticity of Supply (Es) – measures the responsiveness of quantity supplied to changes in price of the good. Shows how sensitive producer are to a change in price.

Es = Percentage change in quantity supplied

Percentage change in price

Es = %∆ in Qs

% ∆ in P

Interpretation of Es:

- Inelastic Supply =‰ Quantity supplied does not respond strongly to price changes. Es is less than one.

- Elastic Supply =‰ Quantity supplied responds strongly to changes in price. Es: is more than one.

- Perfectly Inelastic Supply =‰ Quantity supplied does not respond to price changes at all.

- Perfectly Elastic Supply =‰ Quantity supplied changes infinitely with any change in price.

- Unit Elastic Supply =‰ Quantity supplied changes by the same percentage as the price. Es: is equal to one.

More (or less) elastic supply says that the firms can change supply in larger (or smaller)quantities when price changes.

- Generally, anything that can effect a firm’s ability to change production easily will effect the elasticity of supply.

- the market period occurs when the time immediately after a change in price is too short for producers to respond with a change in quantity supplied. The supply will be perfectly inelastic-supply is fixed and there is no response to the price change.

- the short run implies that the plant capacity will be fixed, but variable costs (labor, materials) can be added to increase production if price rises. Supply will have some degree of elasticity depending on the mix of resource needed to produce, since there can be some change in response to the price change.

- the long run is a time period long enough for the firm to adjust both its fixed plant capacity as well as variable resources. The ability to be responsive means that a smaller price rise can bring forth a larger output increase than in the short run.